COVID-19 Impact : Our team has been closely monitoring the current developments to identify the potential impact of COVID-19 on stakeholders and business processes across the value chain of industries. A special section about COVID-19 will be covered with the report to help companies in defining sustainable strategies.

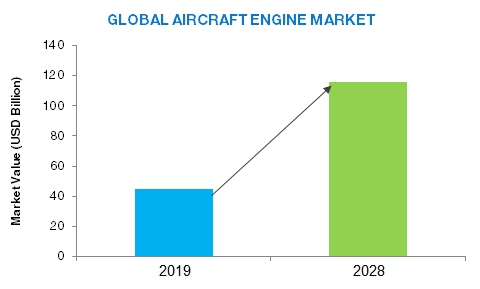

The Global Aircraft Engine Market is projected to reach USD 140.17 Billion by 2028, growing at a CAGR of 6.2% during a forecast period.

Aircraft engines are primary propulsion devices that produce the necessary thrust to generate lift for the aircraft to fly. These engines were synonymous in design to reciprocating engines used in automobiles but in the present world, a shift from reciprocating engines to jet engines has been observed. Turbofan engines are the most common type of jet engines used in commercial aircraft, owing to their high bypass ratio and fuel efficiency. Manufacturers of aircraft engines are continuously engaged in innovating such systems in order to reduce the overall weight and improve fuel efficiency and performance.

Air travel has increased considerably over the years. A large chunk of the population, with high disposable income, now finds traveling through flights an affordable option, which is pushing airline carriers to increase their fleet size to cater to this demand. This factor is one of the primary factors driving the growth of the aircraft engines market as airline carriers are increasingly ordering more and more aircraft. Air pollution caused by the exhaust fumes generated after the combustion of fuel in aircraft engines is a pressing concern acknowledged by government bodies across various economies. Aircraft engine companies are therefore striving to produce fuel-efficient engines that are less polluting. Aircraft engines are cost-intensive products that can be a challenge for both producers and the aviation industry's development. The market is also dependent on the number of orders placed by airline carriers. The high number of orders can strain the productivity of aircraft OEMs, thereby restraining the growth of the market over the forecast period. Additionally, highly skilled personnel are required to manufacture as well as maintain aircraft engines, which increase the cost of investment and consequently, acts as a roadblock to the growth of the aircraft engine market. Stringent regulatory policies and standards are promoting aviation safety and are providing a positive outlook for the aircraft engine market expansion. For instance, in April 2018, the Federal Aviation Administration (FAA) announced the inspections of aircraft operating in the U.S. These encourage industry participants to continuously test and evaluate their engine products appropriately prior to commercializing. New aircraft programs, like Boeing 777X and COMAC C919, are powered by newer generation engines like GE9X and Leap-1C. Such developments in newer generation aircraft are supporting the growth and development of lightweight, advanced propulsion systems.

The turbofan segment holds a major share in the aircraft engines market and may continue to do so during the forecast period. Turbofan engines are most widely used in commercial and military segments. New aircraft programs, like COMAC C919 and Boeing 777X, which are yet to enter service, are powered by newer generation turbofan engine. In 2018, Boeing and Airbus recorded 806 and 800 aircraft deliveries, respectively. With growing aircraft orders in the commercial aircraft segment, which is majorly dominated by the turbofan engine segment, the turbofan engine segment may register the highest CAGR during the forecast period.

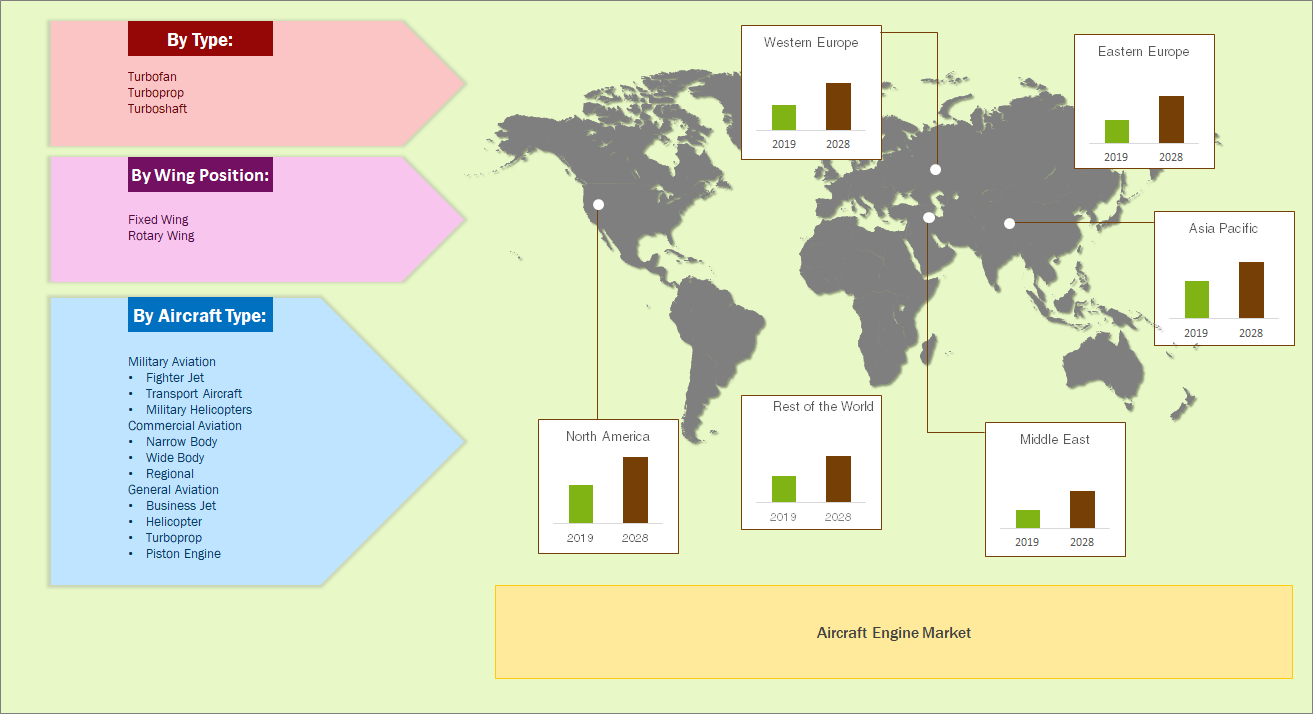

Based on aircraft type, the market is segmented into commercial, military and general aviation. The commercial aviation segment is expected to have the largest market share during the forecast period. With the increase in disposable income and worldwide tourism, a lot of commercial aircraft are being manufactured to meet customer demands. Also, due to globalization, many countries import and export products using air transport. These factors are going to propel the market for commercial aircraft through the forecast period.

The North American region is expected to have the highest share in the market during the forecast period. Two of the biggest aircraft manufacturers, Boeing(US) and Bombardier(Canada) are present in this region and hence is expected to have a lot of demand for aircraft engines. Moreover, the US military expenditure is the highest in the world and the demand for aircraft engines is also high from the military aviation segment. However, with increasing demand for new aircraft in the Asia-Pacific and Middle Eastern countries, Asia-Pacific is anticipated to register the highest CAGR during the forecast period. China and India are expected to be among the major demand generating countries during this period since both these countries are experiencing major growth in their air passenger traffic. Also, the two major aircraft manufacturers, Airbus and Boeing have opened manufacturing plants in China. Moreover, China is expected to overcome the US fleet size within the next four years, in the commercial aircraft segment. Also, the increasing military spending is bolstering the military aircraft developments and procurements, and the growing general aviation fleet in the region is further propelling the growth of the aircraft engine market during the forecast period.

Key Factors Impacting Market Growth:

Key Developments:

What Does This Report Provide?

This report provides a detailed understanding of the global aircraft engine market from qualitative and quantitative perspectives during the forecast period. The report also provides dynamic indicators with potential impact on the market during the forecast period and an in-depth analysis of the leading companies operating in the market.

Market Segmentation:

By Type:

By Wing Position:

By Aircraft Type:

By Region:

Companies Covered: Continental Motors Group, Safran Aircraft Engines, General Electric Co., Pratt & Whitney (United Technologies Corporation), IAE International Aero Engines AG, United Engine Corporation, Rolls-Royce plc, Motor Sich JSC, AVIC Aircraft, Corporation Ltd., Aero Engine Corporation of China, MTU Aero Engines AG, Barnes Group Inc., Honeywell International Inc.

Reasons To Buy This Report:

Customization:

We provide customization of the study to meet specific requirements:

For more information, contact: [email protected]

Single User (PDF)

3850Multi User (PDF)

5150Enterprise User (PDF)

7650Avail customized purchase options to meet your exact research needs.

Detailed scope covering all the major segments in the market

In line data validations to ensure data precision

Market recommendations supporting decision making processes

Round the clock analyst support to resolve your queries

Up to 15% additional free customization to meet your specific requirements